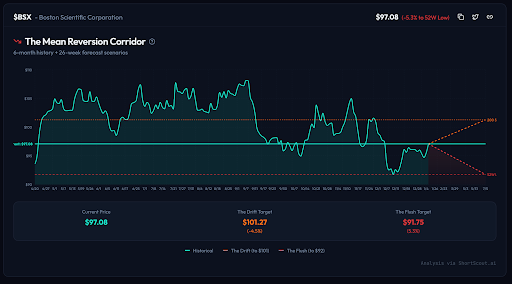

NYSE:BSX

Boston Scientific Corp.

The Thesis: People will continue to have hearts, and they would generally prefer those hearts to beat correctly.

Current Price: ~$95.50 | Target: $125.00+

The Vibe: Growth at a Reasonable Price (GARP), which is a finance term for "buying something good after everyone else panic-sold it."

1. The "Robots Inside You" Angle

If you are a medical device company, your main problem is that biology is messy and difficult. The solution, historically, has been to hire a doctor to poke things with a sharp stick. Boston Scientific’s solution is to build very expensive, very complicated sticks that are essentially robots.

The specific robot everyone is excited about is called FARAPULSE. It uses something called "Pulsed Field Ablation" (PFA), which is a fancy way of saying "zapping the heart with electric fields to stop it from fluttering." The old way of doing this involved burning the tissue (radiofrequency) or freezing it (cryo), both of which have the unfortunate side effect of occasionally damaging things you would prefer to keep, like the esophagus. Not that I know where the esophagus is but, and I am not making this up, I am pretty sure my mom told me to never show my esophagus to a stranger.

But anyway, FARAPULSE just deletes the bad cells without cooking the good ones. It is arguably the biggest leap in cardiac tech since, I don't know, the pacemaker?

This has led to 63% growth in their electrophysiology division, which is the division that deals with "electricity in the body."

The stock is down from its highs (~$109) because markets are efficient and sometimes efficient markets decide that a company growing double-digits in a monopoly-like tech sector should be cheaper for no reason.

2. The "Money Costs Money" Angle

Medical device companies are what finance people call "capital intensive," which means they spend a lot of money. When interest rates come down—as they are projected to do in 2026—this is delightful.

The Rotation: When bond yields fall, asset managers have to find growth somewhere else. Usually, they find it in "companies that sell life-saving technology at high margins."

3. The "Smart Money" Floor

Wall Street analysts have a median price target of $125, which implies a ~30% upside. More importantly, 93% of the stock is owned by institutions. Although the P/E is high, I am a buyer right now at these levels.

The Trade

You are buying a dip in a company that has (1) a technological moat in heart surgery, (2) a tailwind from the Federal Reserve, and (3) a valuation that suggests the market briefly forgot that heart disease is a growth industry.

Current Price: ~$95.50 | Target: $125.00+

The Vibe: Growth at a Reasonable Price (GARP), which is a finance term for "buying something good after everyone else panic-sold it."

1. The "Robots Inside You" Angle

If you are a medical device company, your main problem is that biology is messy and difficult. The solution, historically, has been to hire a doctor to poke things with a sharp stick. Boston Scientific’s solution is to build very expensive, very complicated sticks that are essentially robots.

The specific robot everyone is excited about is called FARAPULSE. It uses something called "Pulsed Field Ablation" (PFA), which is a fancy way of saying "zapping the heart with electric fields to stop it from fluttering." The old way of doing this involved burning the tissue (radiofrequency) or freezing it (cryo), both of which have the unfortunate side effect of occasionally damaging things you would prefer to keep, like the esophagus. Not that I know where the esophagus is but, and I am not making this up, I am pretty sure my mom told me to never show my esophagus to a stranger.

But anyway, FARAPULSE just deletes the bad cells without cooking the good ones. It is arguably the biggest leap in cardiac tech since, I don't know, the pacemaker?

This has led to 63% growth in their electrophysiology division, which is the division that deals with "electricity in the body."

The stock is down from its highs (~$109) because markets are efficient and sometimes efficient markets decide that a company growing double-digits in a monopoly-like tech sector should be cheaper for no reason.

2. The "Money Costs Money" Angle

Medical device companies are what finance people call "capital intensive," which means they spend a lot of money. When interest rates come down—as they are projected to do in 2026—this is delightful.

The Rotation: When bond yields fall, asset managers have to find growth somewhere else. Usually, they find it in "companies that sell life-saving technology at high margins."

3. The "Smart Money" Floor

Wall Street analysts have a median price target of $125, which implies a ~30% upside. More importantly, 93% of the stock is owned by institutions. Although the P/E is high, I am a buyer right now at these levels.

The Trade

You are buying a dip in a company that has (1) a technological moat in heart surgery, (2) a tailwind from the Federal Reserve, and (3) a valuation that suggests the market briefly forgot that heart disease is a growth industry.